BIX ARTICLE

What Is Sukuk?

Jan 08, 2019

|

6 min read

Featured Posts

Social Bonds Illustrative Use-Of-Proceeds Case Studies Coronavirus

Jul 06, 2020

|

2 min read

Sustainable Banking Network (SBN) Creating Green Bond Markets

Jul 06, 2020

|

2 min read

Why is Inflation Making a Big Comeback After Being Absent for Decades in the U.S.?

Mar 24, 2022

|

7 min read

SC issues Corporate Governance Strategic Priorities 2021-2023

Mar 29, 2022

|

3 min read

When you buy bonds, you are essentially loaning money to the issuer for a fixed period. You will receive a predetermined interest rate, which is usually paid annually within that fixed time frame. The value of the bond is repaid at the end of the period and you get your money back. However, because Shariah law prohibits the generation of money from money (such as interest or “riba”), financial instruments that involve the trading and selling of debts, and conventional loan lending (which includes conventional bonds) are not permissible.

This is where Sukuk comes in to fill in the gap between Islamic financing and the global capital market. Sukuk (Arabic: صكوك, plural of صك sakk, "legal instrument, deed, check") is the Arabic name for a financial certificate but can be seen as an Islamic equivalent of bond.

What is Sukuk?

According to Securities Commission Malaysia (SC), sukuk refers to certificates of equal value which evidence undivided ownership or investment in the assets using Shariah principles and concepts endorsed by the Shariah Advisory Council Malaysia (SAC). Accounting and Auditing Organization for Islamic Financial Institution (AAOIFI) described sukuk as securities of equal denomination representing individual ownership interests in a portfolio of eligible existing or future assets.

Think of Sukuk as Islamic bonds that are structured in a way to generate returns to investors and similar to an asset-backed security. They are issued and traded in compliance with the principles of Shariah, which prohibit “riba” or interest.

A sukuk can be structured to offer a fixed return similar to the interest on a conventional bond. But unlike a bond holder, a sukuk holder is granted an ownership interest in the assets or business being financed, and the return is tied to the performance of the underlying assets.

Malaysia’s flexible foreign exchange administration rules allow multilateral development banks, multilateral financial institutions, sovereigns, quasi-sovereigns and local or foreign multinational corporations to issue foreign currency denominated Sukuk in Malaysia.

Sukuk issued by Malaysian government is called Government Investment Issue (GII) and it is used to raise funds from the domestic capital market to finance the Government’s development expenditure. GII is Islamic securities issued in compliance with Shariah requirements and is an alternative debt instrument for the Government. GII is issued under the Government Funding Act 1983 to enable the Government of Malaysia to raise funding in accordance with the Shariah principles. The terms and conditions of the GII are governed by, and construed in accordance with, the laws of Malaysia.

How does Sukuk work?

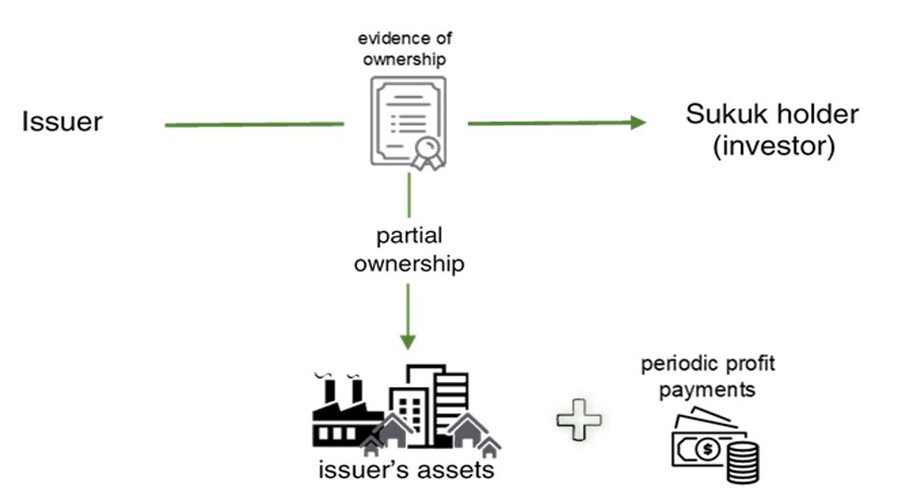

When investors buy Sukuk and become Sukuk holders, they receive a certificate from the issuer as evidence of ownership and are entitled to receive periodic profit payments on the principal amount invested. Upon maturity, the Sukuk holder will get back the principal amount of investment. As with most Islamic financial instruments, there are different methods of achieving the same objective, and the above is just one method of doing it.

For instance, the periodic profit payments may come in the form of profit-sharing or rental from the asset. Different types of sukuk are based on different structures of Islamic contracts (Murabaha, Ijara, Istisna, Musharaka, Istithmar, etc.) depending on the project the sukuk is financing. (For more information on sukuk contract in Malaysia, please visit BIX Malaysia)

Similar to the conventional securities, Sukuk can be rated on a sovereign and corporate basis. The rating analyst or the rating agency will mainly focus on the credit rating of the instrument and any expected default or losses, the agency will give high priority to the legal, the structure and the underlying assets of the Sukuk. It should be noted that, the rating agency will take the Sukuk assets in account only if the assets are in place, otherwise, the rating will be based on the borrower portfolio.

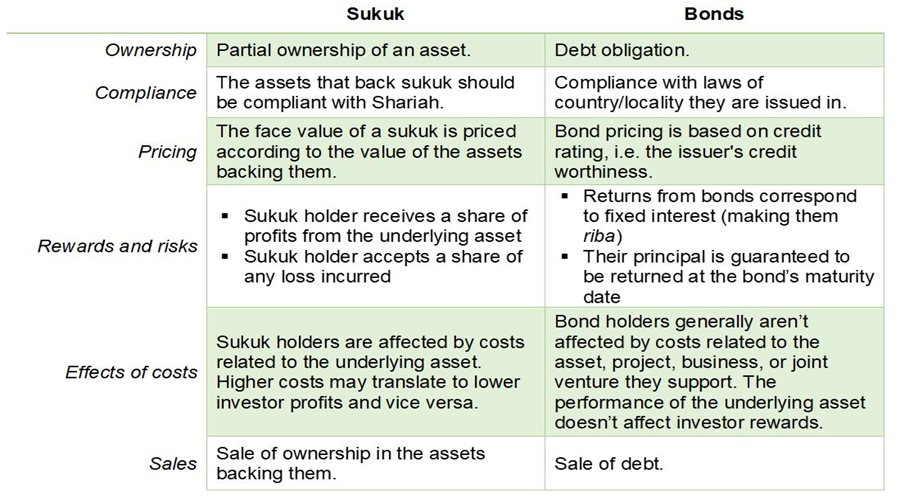

Differences between Sukuk and Bonds

Although some may argue that the differences between sukuk and bonds are merely technicalities, these differences matter to Muslims. In fact, the practice of profiting from money alone, at the expense of productivity and real people has been one of the drivers for many of the economic problems that have plagued the world in the last decade. Interest and artificial inflation of prices based on debt rather than on real value is the main reason why bubbles form, burst, and then lead to recessions and depressions.

Sukuk, unlike bonds, are priced according to the real market value of the assets that are backing the sukuk certificate. Bond pricing is based on the credit rating of the issuer. This is necessary in the case of bonds because when you sell a bond on the secondary market, you are actually selling the debt in the underlying loan relationship. The sale of a sukuk on the secondary market is simply the sale of ownership in the asset.

Evolution of Malaysia’s Sukuk Market

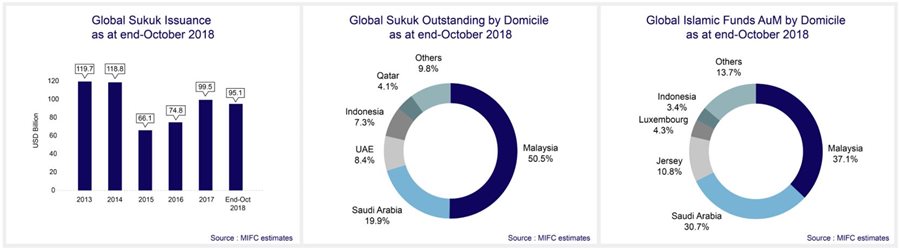

Since the year 1990, where the first corporate sukuk, worth RM125 million, were issued in Malaysia by Shell MDS, the Sukuk market in Malaysia continues to thrive while supported by Malaysia’s conducive issuance environment, facilitative policies for investment activities and comprehensive Islamic financial infrastructure. Malaysia maintained its lead by country with a market share of 28.8% in the first half of 2017. Malaysia recorded RM 138.7 billion (+20.6% y-o-y) of Sukuk issuance as of end-October 2017. The growth was led by increased issuance by quasi-government (+32.2% or RM 38.2 billion), government (+17.7% or RM 46.5 billion) and corporate (+17.7% or RM 54.0 billion) sectors.

Malaysia, being the largest issuer of sukuk globally, is recognised as the most developed Islamic financial market in the world as measured by Thompson Reuters’ Islamic Finance Development Indicator. Malaysia has a deep domestic market that supports local-currency sukuk issuances. Moody’s Investors Service expects sukuk issuance by Islamic financial institutions in Malaysia to grow 10-13% in 2018 and Malaysia will remain a key issuer in south-east Asia. Moody’s also expected Malaysia to continue dominate global sukuk issuance volumes both in the long- and short-term market.

For more information on Malaysia’s sukuk issuance, this can be found using BIX SEARCH tools in BIX Malaysia using 2 easy steps below:

- Click the BIX SEARCH function on the front page

- Filter the function to SUKUK

Contact us at [email protected] for any further question

Link

Disclaimer

This report has been prepared and issued by Bond and Sukuk Information Platform Sdn Bhd (“the Company”). The information provided in this report is of a general nature and has been prepared for information purposes only. It is not intended to constitute research or as advice for any investor. The information in this report is not and should not be construed or considered as an offer, recommendation or solicitation for investments. Investors are advised to make their own independent evaluation of the information contained in this report, consider their own individual investment objectives, financial situation and particular needs and should seek appropriate personalised financial advice from a qualified professional to suit individual circumstances and risk profile.

The information contained in this report is prepared from data believed to be correct and reliable at the time of issuance of this report. While every effort is made to ensure the information is up-to-date and correct, the Company does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information contained in this report and accordingly, neither the Company nor any of its affiliates nor its related persons shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

YOU MAY ALSO LIKE

ARTICLE

Jun 04, 2026

|

4 min read

ARTICLE

May 11, 2026

|

6 min read

ARTICLE

May 04, 2026

|

4 min read

ARTICLE

Mar 02, 2026

|

4 min read