BIX ARTICLE

Malaysia To Issue Samurai Bond

Nov 12, 2018

|

6 min read

Featured Posts

Social Bonds Illustrative Use-Of-Proceeds Case Studies Coronavirus

Jul 06, 2020

|

2 min read

Sustainable Banking Network (SBN) Creating Green Bond Markets

Jul 06, 2020

|

2 min read

Why is Inflation Making a Big Comeback After Being Absent for Decades in the U.S.?

Mar 24, 2022

|

7 min read

SC issues Corporate Governance Strategic Priorities 2021-2023

Mar 29, 2022

|

3 min read

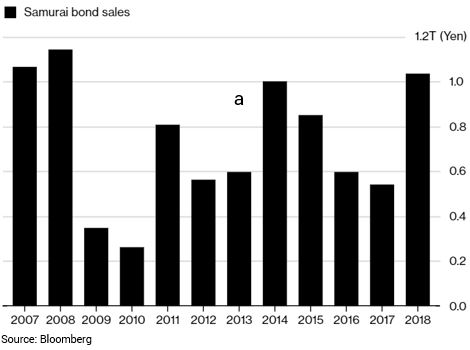

The Japanese Government has agreed to guarantee the JPY200 billion (RM7.4bill) 10-year Samurai bond issuance of Malaysia government at 0.65% coupon which was announced during Malaysia’s 2019 budget This article will look into what is Samurai bond and what is the advantage/disadvantage in issuing Samurai Bond.

This offer may look attractive with its 0.65% coupon which is much lower than Malaysia Government Securities (MGS) 10-year maturing 6/2028 coupon 3.73%.

However, Malaysia need to repay back the principal at the end of maturity in Japanese Yen and there is no guarantee that the level of the yen will remain the same 10 years later. Even if the government hedge the future currency exchange, the premium government paid may resulted in the effective interest to exceed current MGS coupon level. Nonetheless, there are other attractive feature of issuing Samurai Bond besides its attractive low coupon.

What is a ‘Samurai bond’?

Samurai bonds give issuers the ability to access investment capital available in Japan. The proceeds from the issuance of Samurai bonds can be used by non-Japanese companies to break into the Japanese market, or it can be converted into the issuing company's local currency to be used on existing operations.

Why Malaysia issuing Samurai Bond?

This news is significant as some of the Malaysia’s foreign denominated government guarantee (GG) bond are issued at 5.99% coupon which is much higher compared to local currency GG bond such as 10-year Prasarana GG bond below last traded at 4.39%.

Source: BIX Malaysia

Source: BIX Malaysia

Looking at liquidity and demand for Malaysia Samurai Bond, the Japanese government has agreed to guarantee the issuance through its Japan Bank for International Corporation. Therefore, Japan’s local investor bear not much risk from holding government guarantee samurai bond other than its own sovereign risk. Its is expected the issuance of Malaysia Samurai Bond will be accepted with open arms by the local Japanese investors and other foreign investors in the Japanese bond market.

The benefit of issuing Samurai Bond for Malaysia is the access to the bigger investor base and relatively low interest rate. However, Malaysia as an issuer must be careful of the currency risk. Malaysia as an issuer need to repay back the principal at the end of maturity in Japanese yen and there is no guarantee that the level of Yen will remain the same 10 years later. This mean Malaysia may need to pay more than expected if the Japanese yen strengthen 10 years later when the bond reach maturity.

Advantages and Disadvantages of Samurai Bond

| Advantages | Disadvantages |

|---|---|

|

|

Is this Malaysia’s first time issuing Samurai Bond?

Other foreign bonds include Kangaroo bonds, Maple bonds, Matador bonds, Yankee bonds, and Bulldog bonds.

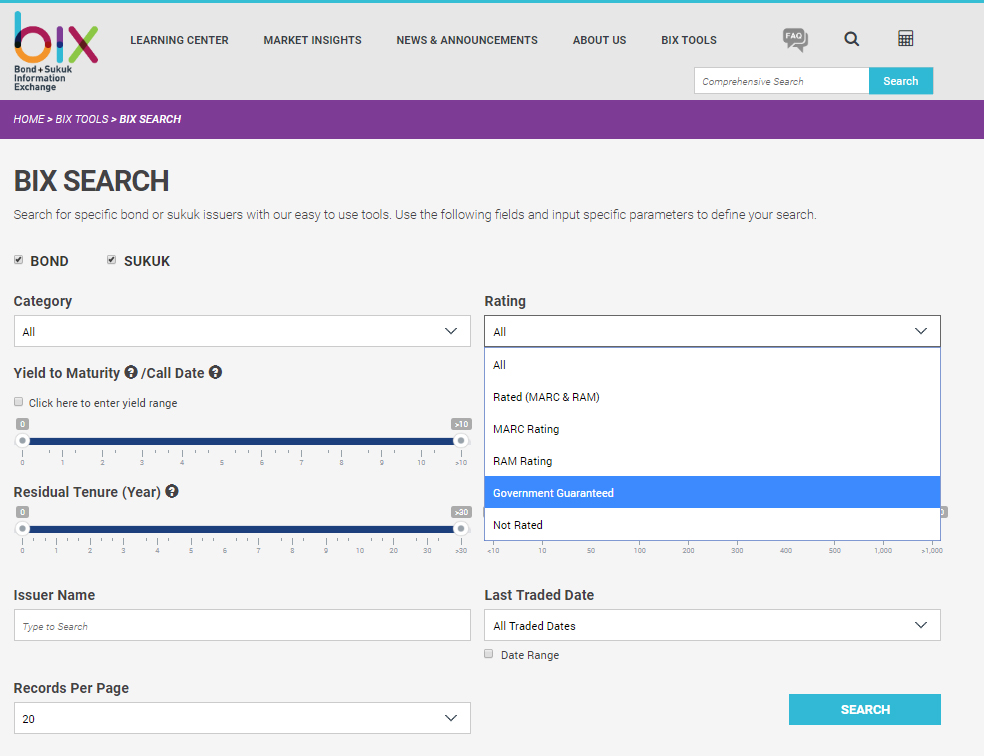

For more information on Malaysia’s government guarantee bond and sukuk, this can be found using BIX SEARCH tools in BIX Malaysia website (www.bixmalaysia.com) using 2 easy steps below:

- Click the BIX SEARCH function on the front page

- Filter the rating function to Government Guaranteed

Disclaimer

This report has been prepared and issued by Bond and Sukuk Information Platform Sdn Bhd (“the Company”). The information provided in this report is of a general nature and has been prepared for information purposes only. It is not intended to constitute research or as advice for any investor. The information in this report is not and should not be construed or considered as an offer, recommendation or solicitation for investments. Investors are advised to make their own independent evaluation of the information contained in this report, consider their own individual investment objectives, financial situation and particular needs and should seek appropriate personalised financial advice from a qualified professional to suit individual circumstances and risk profile.

The information contained in this report is prepared from data believed to be correct and reliable at the time of issuance of this report. While every effort is made to ensure the information is up-to-date and correct, the Company does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information contained in this report and accordingly, neither the Company nor any of its affiliates nor its related persons shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

YOU MAY ALSO LIKE

ARTICLE

Jun 04, 2026

|

4 min read

ARTICLE

May 11, 2026

|

6 min read

ARTICLE

May 04, 2026

|

4 min read

ARTICLE

Mar 02, 2026

|

4 min read