BIX ARTICLE

Malaysia Bond And Sukuk: Quarterly Report 1Q 2018

May 14, 2018

|

5 min read

Featured Posts

Social Bonds Illustrative Use-Of-Proceeds Case Studies Coronavirus

Jul 06, 2020

|

2 min read

Sustainable Banking Network (SBN) Creating Green Bond Markets

Jul 06, 2020

|

2 min read

Why is Inflation Making a Big Comeback After Being Absent for Decades in the U.S.?

Mar 24, 2022

|

7 min read

SC issues Corporate Governance Strategic Priorities 2021-2023

Mar 29, 2022

|

3 min read

1Q of 2018 saw the bond investor globally on the edge as the UST start the year with a selloff in bonds but managed to stabilize later and recover some of the losses. 10y UST, 10y UK Gilt and 10y German Bund yields rose 33bps, 16bps and 7bps respectively.

OVERVIEW

Malaysian sovereign bonds were generally well-supported despite Bank Negara raising the OPR by 25bps. The buying interest may persist with anticipation of no rush in rate hikes by BNM and stable MYR below RM4.00. However, volatility was high in March on concerns over increased interest rates globally for the rest of the year.

Bank Negara Malaysia kept rates steady at 3.25% at the March MPC and sound positive on the domestic factor while raised cautions on possible financial market swing and prospect of trade friction externally.

GOVERNMENT BOND & SUKUK

While inflation stays soft and Bank Negara not rushing for another hike this year, we see gains in MYR bonds particularly alongside recovery in UST. Also, Fed stance appears to be less hawkish in March FOMC, may pressure USD further which could trigger renewed foreign inflows and provide a lift to MYR bonds in medium term.

Total Government bond matured during the quarter is RM18.50 billion while new and reopening auction issued at RM30.50 billion. The take up in January was decent with 5-year GII 04/22 reopening btc at 2.581x but saw the take up softer starting on the second half of 1Q2018.

Demand of MGS 11/21 which will be the new benchmark for MGS 3 year was soft at BTC 1.722x. The lower demand may due to existing MGS 07/21 at RM13.5b, MGS 09/21 at RM11.7b and MGS 2/21 RM8.0b still available.

For 2Q2018, there are only 1GII maturity at RM7.5b and no MGS maturity while in the pipeline will be 5 GII and 4 MGS auction.

CORPORATE BOND & SUKUK

Malaysia’s corporate bond and sukuk start the 1Q2018 well with a strong issuance of RM29.6b which is up 7% from last year and is the strongest start for the year on the corporate side over the past 6 years. The improvement in issuance was mostly in March as the bond market sentiment recovered with stable local bond performance amid the OPR hike and stronger Ringgit compared to last year.

The major issuer is mostly from the infrastructure sector such as Edra Energy (RM5.1b) to finance 2,242 MW gas power plant in Melaka, Danainfra (RM4b) to construct MRT2 and Prasarana (RM3.b) for LRT 3.

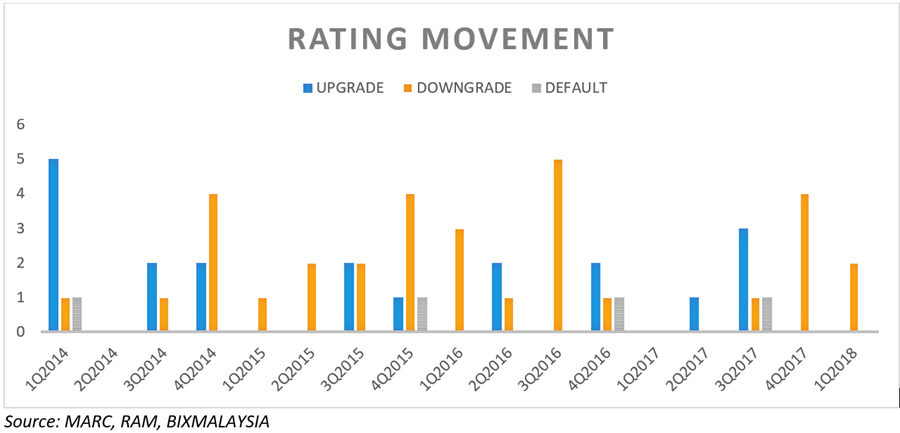

On the credit side, 1Q18 recorded 2 rating downgrades. RAM cut Smart Holdings’ rating to A1 from AA2 as traffic decline at SMART Tunnel did not abate and had reduce cashflow and weaken debt service metrics. The other downgrade comes from Lafarge Malaysia Bhd’s subsidiary, Lafarge Cement whose rating dropped 2 notches to A1 (by RAM) due to a sharp fall in financial performance as tepid demand and overcapacity kept pressure on cement prices.

2Q OUTLOOK

The main highlight for 2Q2018 will be the General Election 14. Based on the last election, the bond market rally post-election as the political uncertainty is very high pre-election. Furthermore, the last election happened before QE taper in the US where foreign investor and offshore bank fast money is available. Looking at short term, the MGS may improve slightly if Ringgit continue to strengthen against USD despite global theme for bond yield to rise but not due to election.

The new retail bond framework by Securities Commission is also expected to be launch on the 2Q of 2018. The new bond and sukuk framework will widen the investor base and hopefully increase the liquidity in the secondary market in Malaysia.

Download Report

Disclaimer

The information contained in this report is prepared from data believed to be correct and reliable at the time of issuance of this report. While every effort is made to ensure the information is up-to-date and correct, the Company does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information contained in this report and accordingly, neither the Company nor any of its affiliates nor its related persons shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

YOU MAY ALSO LIKE

ARTICLE

Jul 10, 2026

|

7 min read

TUTORIAL

Apr 08, 2026

|

7 min read

ARTICLE

Jan 09, 2026

|

7 min read

ARTICLE

Oct 08, 2025

|

7 min read